In the weeks leading up to the June 23 Brexit referendum, the Bank of England warned that a vote to leave the European Union could result in a recession, raising fears that housing prices could plummet.

Yet in the months following the controversial vote, inflation rates have stabilised and housing prices have slowly risen. Between May and August, housing prices increased by a total of 0.87%, with growth rates of approximately 0.15% each month. And as described below, a 0.063% decrease in September may have nothing to do with the referendum.

Naysayers have lauded these factors as evidence that recession fears were baseless.

But the analysts at Tranio.com believe that it is still too early to determine what impact the Brexit referendum has had on the British economy and London housing prices.

In this article, we explore several key issues to keep an eye on in the post-Brexit housing market. While we focus primarily on London, we also consider housing price trends across the rest of the United Kingdom.

Recession and housing price declines: echoes of 2008

Many who are wary that the Brexit referendum will bring about a recession and housing price decline are haunted by memories of the troubles the British market experienced amid the 2008 global financial crisis. However, a closer look at the numbers reveals that fears of history repeating itself may be unfounded.

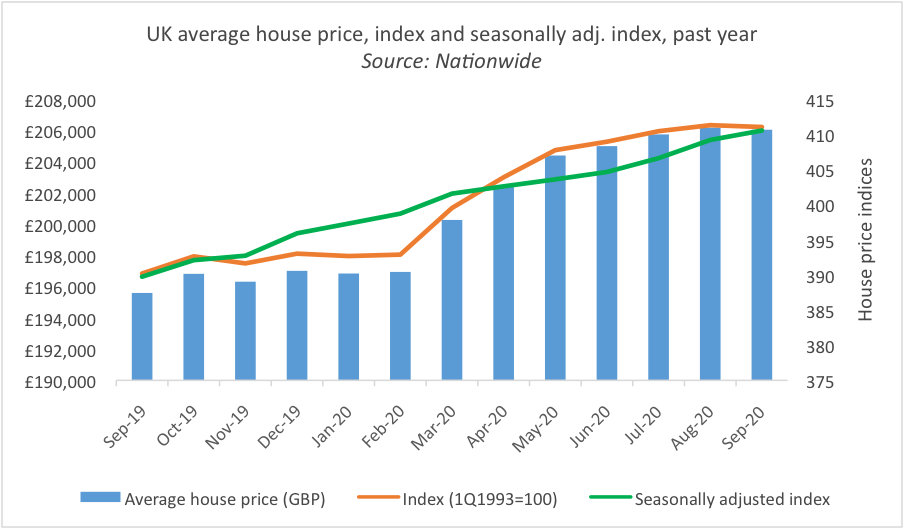

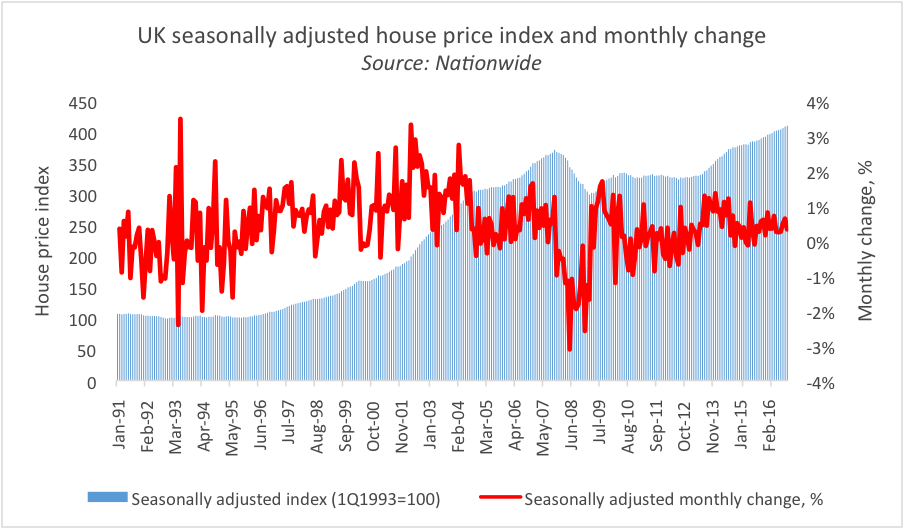

To gauge housing price trends from the past three decades, we obtained data from Nationwide Building Society, a respected British financial institution. This data, illustrated in the table below, revealed that with the exception of the period surrounding the financial crisis, housing prices across the United Kingdom have generally experienced steady growth since the early 1990s.

The housing price index experienced a precipitous and protracted decline in late 2007 and early 2008. This slump coincided with the United Kingdom’s general economic decline; it was in the second quarter of 2008 when British authorities first formally acknowledged the recession.

In contrast, no macro-level indicators presently suggest that the United Kingdom will suffer a recession in the coming months. Forecast data from the UK Office for National Statistics holds that the British economy will not contract until the third quarter of 2017, and that this contraction is only expected to affect that quarter.

Notably, this is subject to debate. A number of economists and observers predict a delayed recession. British think tank the National Institute of Economic and Social Research said that the UK faces a 50% chance of entering a recession by 2018, The Guardian reported in August.

Furthermore, the UK housing price index was characterised by volatility in the 1990s and 2000s. However, it has remained relatively stable since 2013.

This stabilisation in month-to-month changes in the Nationwide index – which has pushed no lower than 0.1% since January 2013 and has remained positive since July 2015 – points to generally uninterrupted, albeit slow, growth.

Statistics on year-on-year percentage growth additionally show an upward trend in the index, consistently reflecting growth since March 2013.

Key takeaway: Parallels between the UK property market in 2008 and 2016 are generally misleading.

The seasonality factor

Across the United Kingdom, housing prices dipped slightly in September. However, this dip may not reflect an overall decline; rather, it may point to seasonality.

In general, the UK housing market is subject to seasonality. Specifically, prices tend to pick up each year between March and April, and tend to settle or slump between fall and mid-winter of each year, typically between October and December.

While the September price dip could be linked to the Brexit referendum, it could also simply be a manifestation of the market’s annual seasonality pattern. Only further statistics for October, November and December will elicit the true nature of the trend.

One thing is already certain: the seasonally adjusted index shows steady growth throughout the year, including the immediate pre-referendum and post-referendum months; when more data for the coming months becomes available, the index trend will adjust.

Key takeaway: Housing price patterns documented since the Brexit referendum may be attributable to seasonality.

While it may be tempting to attribute all 2016 UK housing price trends to the Brexit referendum, doing so would be short sighted in light of several other key developments. The latter include increased stamp duties and declining mortgage lending.

Since April, purchasers of buy-to-let properties have been required to pay an extra 3% stamp duty.

This policy was developed to address two issues: on one hand, first-time buyers were feeling increasingly barred from the market, and on the other, rental rates were skyrocketing.

The intended long-term effect of this policy was to edge buy-to-let investors out of the market in order to make way for first-time buyers, especially in markets where supply has trailed demand.

However, the policy’s impact on sales volumes remains to be seen. While it may succeed in boosting first-time purchases, it could also have a negative net result given that it penalises second-home buyers.

According to quarterly data issued by the Bank of England Prudential Regulation Authority and the Financial Conduct Authority, mortgage lending was already declining before the referendum. Specifically, gross advances decreased by 9.3% between the first and second quarters of 2016. The stamp tax increase for buy-to-let properties may be a key factor behind the mortgage decline.

Notably, in August the Bank of England moved to counter the mortgage decline by lowering the base interest rate from 0.5% to 0.25%, the first decrease in seven years, and issued £60 billion in long-term government bonds. As these measure aimed to further stimulate lending and stave off a potential recession, they could turn the mortgage lending decline around.

Finally, while it is possible that the referendum had a chilling effect on property purchases by fostering a climate of uncertainty, concrete Brexit policies, such as those related to trade deals and visa regimes with EU countries, will likely have a more significant and enduring impact than the referendum itself. As these policies are currently being developed, they are unlikely to have a substantial impact on 2016 housing prices.

Key takeaway: Any housing price analysis will need to take into account the referendum, the stamp tax, the mortgage decline and the interest rate decrease, both individually and in tandem with one another, in order to gauge their true combined impact on the 2016 property market. We will have to wait to obtain mortgage lending data for the rest of the year before we can properly undertake such an analysis.

For years, London has boasted the highest housing prices in the United Kingdom. This is largely attributable to a well-documented supply issue.

Savills reported in the Autumn 2016 edition of its Spotlight Prime London Residential Markets report that, between 2011 and 2015, prime new build sales surpassed construction completion rates by an average ratio of more than 2:1.

However, according to Savills, in the first half of 2016 and after about two years of converging sales and construction, prime market sales volumes fell and construction completions rates rose significantly, reaching a ratio of about 1:1. In light of this, developers are facing pressure to lower prices, which could in turn stifle construction.

The supply issue is likely a key reason that prices have continued growing for most of London’s housing segments despite the uncertainty surrounding the Brexit referendum.

And the problem doesn’t appear to be on its way out: the UK construction sector has recently experienced acute skill shortages, and close to 5% of the sector’s work force comes from EU member states. The construction sector is one of several that are extremely sensitive to changes in investor confidence and macro-level economic and political shifts, which means that continued torpor in the building of new homes and flats is expected.

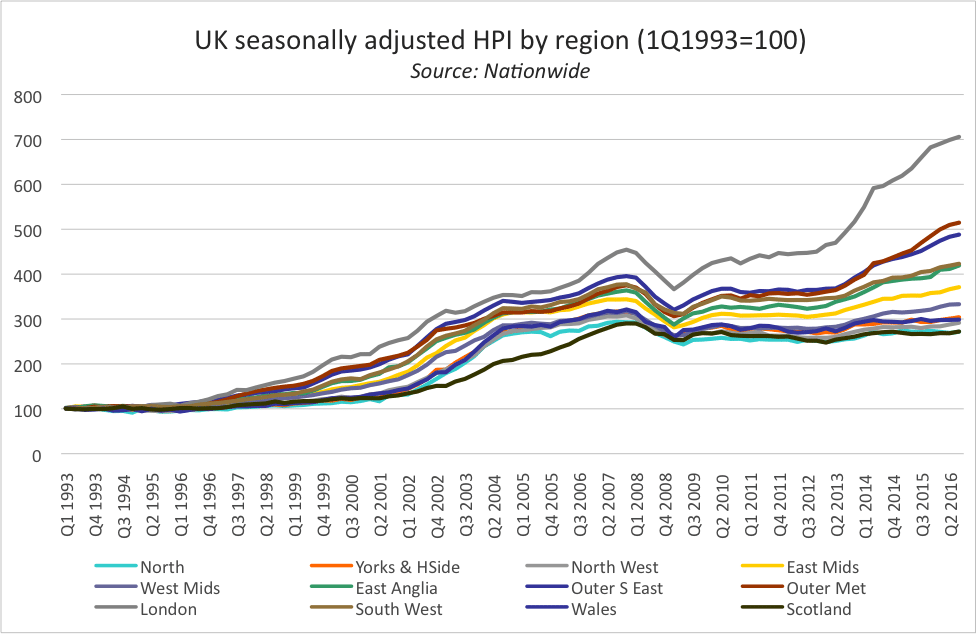

As shown in the graphs below, London property prices have soared past those of all other parts of England and most other parts of the United Kingdom since 2008. As the economy began to strengthen in 2013 and 2014, house prices across much of the UK began to follow suit.

The graph below depicts regional growth rates across the United Kingdom, excluding Northern Ireland.

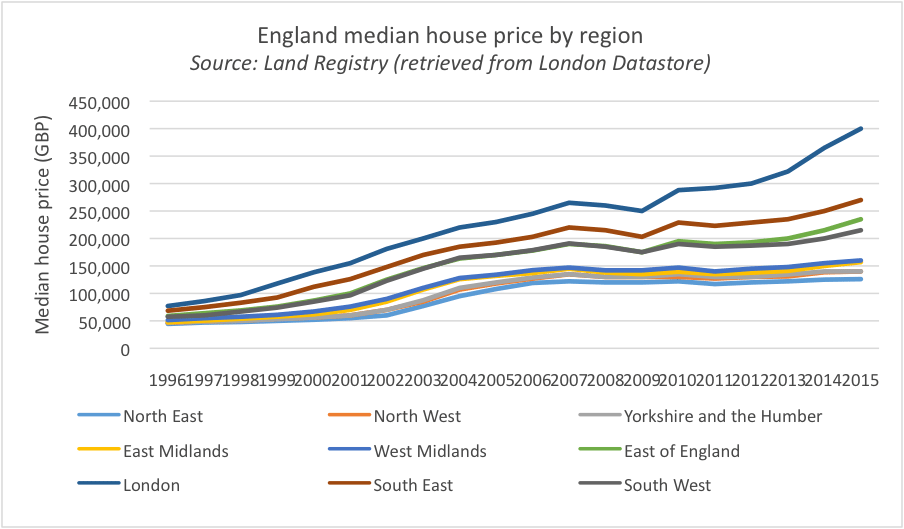

The following chart depicts median house prices of England’s regions.

Key takeaway: Generally speaking, supply is expected to remain problematic across most London real estate sectors. As such, high demand and inadequate supply are expected to continue to buoy housing prices in the city despite Brexit fears.

Amid the volatility of the pound in recent months, many domestic investors have begun to pull out of real estate transactions in London or refrain from making new purchases. Likewise, investors from EU countries have been wary of purchasing UK properties amid Brexit uncertainties, particularly those related to potential immigration and trade barriers.

However, demand remains strong among foreign buyers from countries outside of the EU, where Brexit fears are limited and the weaker pound provides a strong incentive to buy quickly.

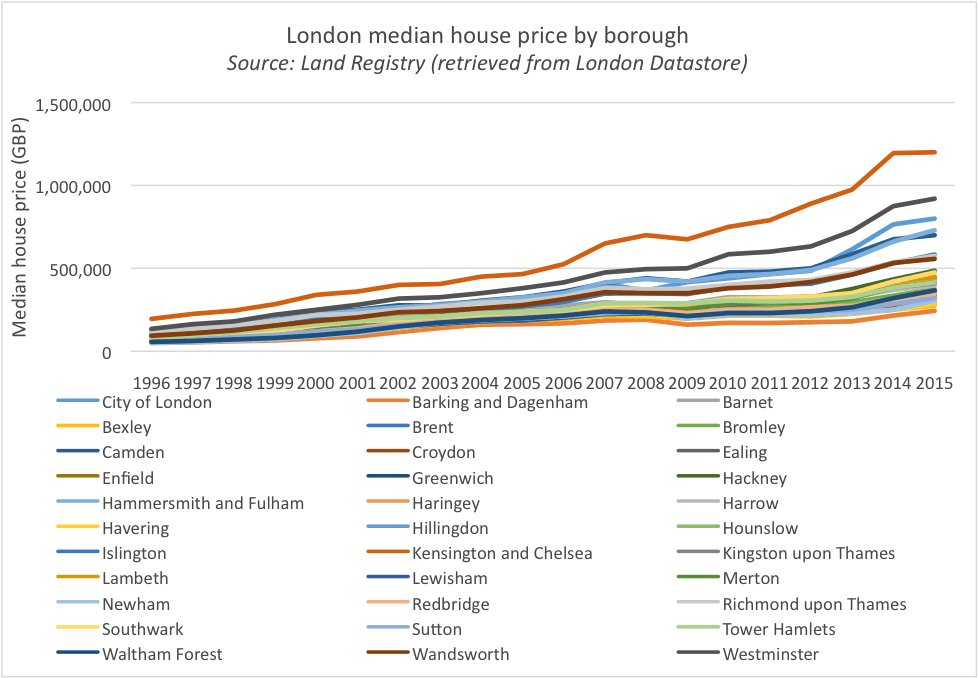

In 2016, roughly 40% of London’s inhabitants are immigrants; in some areas, such as Mayfair and the West End, about 55% of real estate market activity is driven by investment from nationals of India, Russia and countries across Africa and the Middle East. From 2012 to 2015, about 20% of property purchases in Kensington and Chelsea, arguably London’s poshest borough (see chart below), were made by foreign nationals.

A study by Savills concluded that, in 2013 and 2014, about 32% of all prime property buyers in the British capital were foreign nationals, with roughly half of that group (16.5%) coming from EU member states.

The Financial Times reported in July 2013 that foreign investors were behind as much as 82% of all property activity in London at the time.

The post-referendum market has experienced a surge in requests from overseas buyers hailing from the Middle East, East Asia and other distant regions. While EU investors still seem to hold some level of interest in London’s market, investors from outside the EU appear fervent to take advantage of the weakening British pound and declining house prices in the prime property market.

Some of the recent and current investment inflows have even been directed at the redevelopment of former industrial and similar non-residential properties. A prime example of this is the £8 billion redevelopment project at the Battersea power station, a project backed by a consortium of Malaysian property development and investment companies.

The large-scale renovation project is aimed at repurposing the facility for several uses – including residential, retail, and office functions – attracting a new wave of entertainment-industry firms and various other businesses, including the tech giant Apple.

This redevelopment project will likely raise housing prices in the Wandsworth and Lambeth boroughs; apartments in the immediate vicinity of the power station are expected to range between half a million and 20 million pounds upon the project’s completion.

In light of the larger pre-referendum rise in London housing prices and their precarious post-referendum status, London mayor Sadiq Khan said that he would conduct “the most thorough research on [the matter of foreign property ownership] ever undertaken,” The Guardian reported in late September.

“It’s clear we need to better understand the different roles that overseas money plays in London’s housing market, the scale of what’s going on, and what action we can take to support development and help Londoners find a home,” The Guardian quoted Khan as having said.

Among other aims, the inquiry will strive to increase transparency with respect to property ownership in London. At this stage, it’s too early to determine whether the outcome of the inquiry will have any impact on the foreign property purchasing patterns outlined above.

Key takeaway: Demand for London property is strong among foreigners from non-EU countries. Such purchasers are eager to take advantage of the weaker pound, and are not deterred by the uncertainty that looms over would-be EU purchasers. While it is possible that Khan’s inquiry could eventually deter foreign purchasers from flocking to London, at this stage it is too early to tell.

Thomas H. Espy, Tranio.com