David Kauders FRSA a founder member of Kauders Portfolio Management AG, has been hailed in the financial press as a “radical thinker”. Here, he puts forward three radical thoughts that fill a glaring omission in economics and finance.

Keynesian policies of credit creation are fashionable, but they create debt which cannot expand to infinity. The question of how much debt the world can actually afford is rarely addressed.

British pundits have recently argued that government debt can run at 100% of GDP (gross domestic product) using the 1945 peak of 250% of GDP as justification. This is misguided. In 1945, private debt was insignificant whereas today, business and household debt is around three times the value of outstanding government debt ‒ and far more costly.

I call the limit to the growth of total debt in society The Financial System Limit in my new book of the same name. It is fairly easy to prove the existence of such a limit in logic because the world would need an unlimited supply of goods and services to pay the infinite interest that would follow from debt reaching infinity. Since money today is book-entry based on credit, the world’s stock of credit equals the world’s money ‒ and equals the world’s debt.

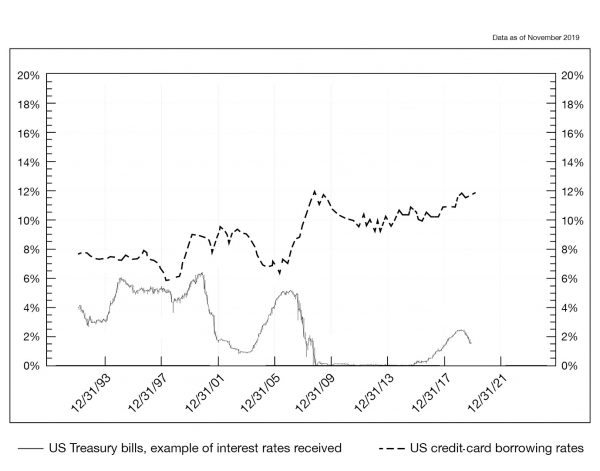

Why do households pay high rates to borrow when governments can borrow at 0.2% for ten years, and depositors earn nothing on their deposits? The striking graph of credit card rates compared to LIBOR (London Inter-Bank Offered Rate) – a proxy for deposit rates – which appears in my book (and is the basis for the cover design) is reprinted below. It demonstrates that the gulf between deposit and borrowing rates has widened steadily. Why? Because businesses and consumers are paying for bank compliance costs and squeezed bank margins.

In the absence of academic research to establish the cost to society of this gulf between deposit and paid interest rates, I set out to make estimates. While I can hope that a future research project will establish more accurate figures, my estimate shows that, prior to the pandemic, the world was spending about US$ 17 trillion annually on interest. This was a fifth of world economic output.

The pandemic will have driven the interest expense up, more through business and household borrowing at high rates rather than cheap government borrowing. The pandemic has also reduced economic output, to be compounded in Britain’s case by Brexit. The proportion of world economic output spent on interest is rising. Is this dangerous?

The first part of my book sets out three radical thoughts. First, the existence of such a financial limit is demonstrated. This is followed by an estimate of the economic output devoted to interest. The third radical thought is that the business cycle we knew has been supplanted by a central banking cycle. Each recession is neutered with a dose of stimulus, the dosage rising with every turn of the economic cycle. The stimulus brings immediate relief but adds to debt servicing costs, thereby inducing the lethargy from which the next, deeper, financial crisis can emerge, perhaps a decade later. There is a short-term benefit from escaping each crisis, which is nullified by the long-term real cost of additional ongoing debt interest payments.

Academic theory pursues irrelevances. Finance schools encourage budding finance professionals to borrow in order to exploit the tax efficiency of debt. Some economists describe central bank money printing – known as ‘quantitative easing’ – as the way the world works. True, but that doesn’t make it right. Others are stuck in the futile debate between sound money and credit creation.

Proposed solutions are little help. Here is an example: “helicopter money”, where a large sum of money is printed and given to the public, is supposed to stimulate spending. What actually seems to happen is that those with debts pay debt down, while those with assets add to their savings. This behaviour shrinks the economy rather than boosting it. The pandemic is likely to bring a similar behaviour change. As unemployment rises, over-borrowed households will simply cut their spending, move somewhere cheaper, or even default on their debts. Such forces are deflationary. No amount of stimulus can neuter deflation.

The state of the economy and capital markets also raises deep questions about pensions. Lack of resources to pay pensions is likely to become a continuous deflationary pressure.

As to where the financial system limit lies, it may vary by country. I examined two case studies, one of a country in default (Puerto Rico); the second of a major company in default (British construction firm, Carillion). With one-fifth of economic output devoted to interest, it seems the world is already half-way to the financial system limit.

Part of the problem is that there are glaring contradictions in existing economic policies:

- Refusing to stimulate our way out of recession is seen as foolish. Yet adding to the money already wasted on interest is equally so. The choice seems to be: foolishness now versus deferred foolishness when the interest cost has mounted further.

- Existing policies no longer work. Instead of debating stimulus versus austerity, or lower interest rates versus fighting inflation, economists and politicians need to think about how to get debt levels and their associated interest costs down.

- Public services, taxation, public borrowing and regulation are in a four-way contradiction: it is impossible to meet the requirements of all four. Taxation incurs dead-weight costs of administration while public expenditure encourages marginal use of scarce resources. Politicians like to boast about public services but realise that rising taxes and increased regulation are unpopular.

- Limited immediate relief may only be possible through redistributive taxation and simplifying compliance demands on banks; and

- Experiments should be carried out with subscription by the people, to development aid and economic support.

These points will only have a minor effect on the deflationary debt trap the world faces. The tragedy is that the authorities do not admit to the trap. The farce, that their policies worsen it. New thinking needs to allow alternatives to the present debt-based financial system to emerge.

The Financial System Limit by David Kauders will be published by Sparkling Books as an eBook on 27th July, priced £4.99. It is now available for pre-order on Amazon or Kobo. For more information, or links to additional retails worldwide, visit Sparkling Books.

Q and A with David Kauders

We speak to investment manager and author David Kauders about his radical thoughts on global finance and why there are no easy answers to escaping economic deflation in a post-coronavirus world.

Q. Why has the economics profession, and likewise governments, not noticed any connection between interest paid and GDP?

A. It is possible that somebody has realised the connection and I simply overlooked their work. But the main problem is that academic economics has turned into a formula-based examination of details rather than a broad process of thinking about issues. As for governments, they think only of themselves. Look at all the commentary about the cost of government debt in the United Kingdom: it says nothing about the far higher cost of business and household debt.

Q. Do bank compliance costs also explain why deposit interest is low or non-existent?

A. Deposit rates have been forced down by central bank actions. There is a cost effect on deposit rates, but in my view the overall costs of running banks matter more to borrowers.

Q. You say in the book that wealth is difficult to tax because asset sales depress prices. Surely the same applies to income? Won’t taxing income, even just higher earners, therefore hit spending and defeat the intended purpose?

A. Surplus income that can be taxed occurs with high earners, not the broad middle ground. High earners are the ones who can save most, so their spending would be hit proportionately less than by taxing middle earners.

Q. If the whole world is heading towards Puerto Rican-style debt problems then will tax rises, your minor banking changes, and raising new equity actually achieve anything?

A. I admit the effect will be limited, but something is better than nothing. The problem of buying short-term gains at the expense of longer-term losses is not new. Sooner or later, difficult issues have to be faced. When it becomes obvious that economies cannot recover completely from the pandemic then politicians may start to face the deflationary problem.

Q. Does your theory mean that stimulus should be abandoned when the next economic problem hits?

A. Stimulus should be a last resort, not the first port of call. It’s one thing governments borrowing cheaply for a short time, but they then use the funds to encourage more bank and consumer lending, which is far more expensive.

Q. Your argument in the book that bank loan losses are low was valid before the pandemic, but loan losses are now going to be much higher. Have banks simply been squirrelling money away for a rainy day?

A. There have been efforts to raise bank capital standards and hence banks have been encouraged to provide for more loan losses. It’s prudent accounting.

Q. There will always be some politicians (or autocrats) somewhere for whom international cooperation is unwanted. Therefore the world does not face a choice of cooperation or self-isolation, as you say in the book. Cooperative solutions cannot work. Do you agree we should look after ourselves first?

A. When did isolation and self-interest lead to better economic outcomes? That is hardly the case in North Korea. The problem of excessive debt cannot be solved in isolation because some debt is cross-border.

Q. You rule out many recognised solutions such as helicopter money, debt to equity conversion and increased IMF (International Monetary Fund) drawing rights, but some of them work some of the time. If you put those bits together then surely there will be some debt reduction, making your argument too extreme?

A. The assumptions underlying much economic theory are out of date. Helicopter money will fail because people will choose to pay down debt or save more in preference to spending. IMF drawing rights are part of the problem of excess debt creation. Debt to equity conversion can work on a limited scale but raises contradictions about who benefits by release from debt obligations. These contradictions will need political solutions.

Q. Given the bleak outlook, should businesses simply give up now?

A. Absolutely not. Many will need to slim down, and those dependent on consumers spending borrowed money will need to slim down the most. It’s likely that many businesses will handle lower volumes of goods or services at higher prices, with an overall shrinkage in sales value. This is a period of great change and some smart businesses will take advantage of opportunities. For examples, look at the spread of Zoom and the commercial acumen of Ethiopian Airlines growing its freight business.

Q. There are supply chain bottlenecks that are causing inflation and shortages now: cargo costs, grain distribution. Can these offset the deflationary forces?

A. There will be price rises, particularly in the food chain and transport, but the volume shrinkage will outweigh these.